How Elite Cycling Recon Tactics Can Shape Your Savings Strategy

As proud partners of Team Picnic PostNL, we know that elite cyclists have to constantly adjust to changing terrain to maintain their momentum. The same principle applies to your money. Leaving cash idle in low-interest accounts may mean missing out on higher returns, while making small, tactical adjustments could help your savings work harder.

The overview

Here is a summary of the key points featured on this page, which you can save or screenshot for future reference. Read on for more information on each area.

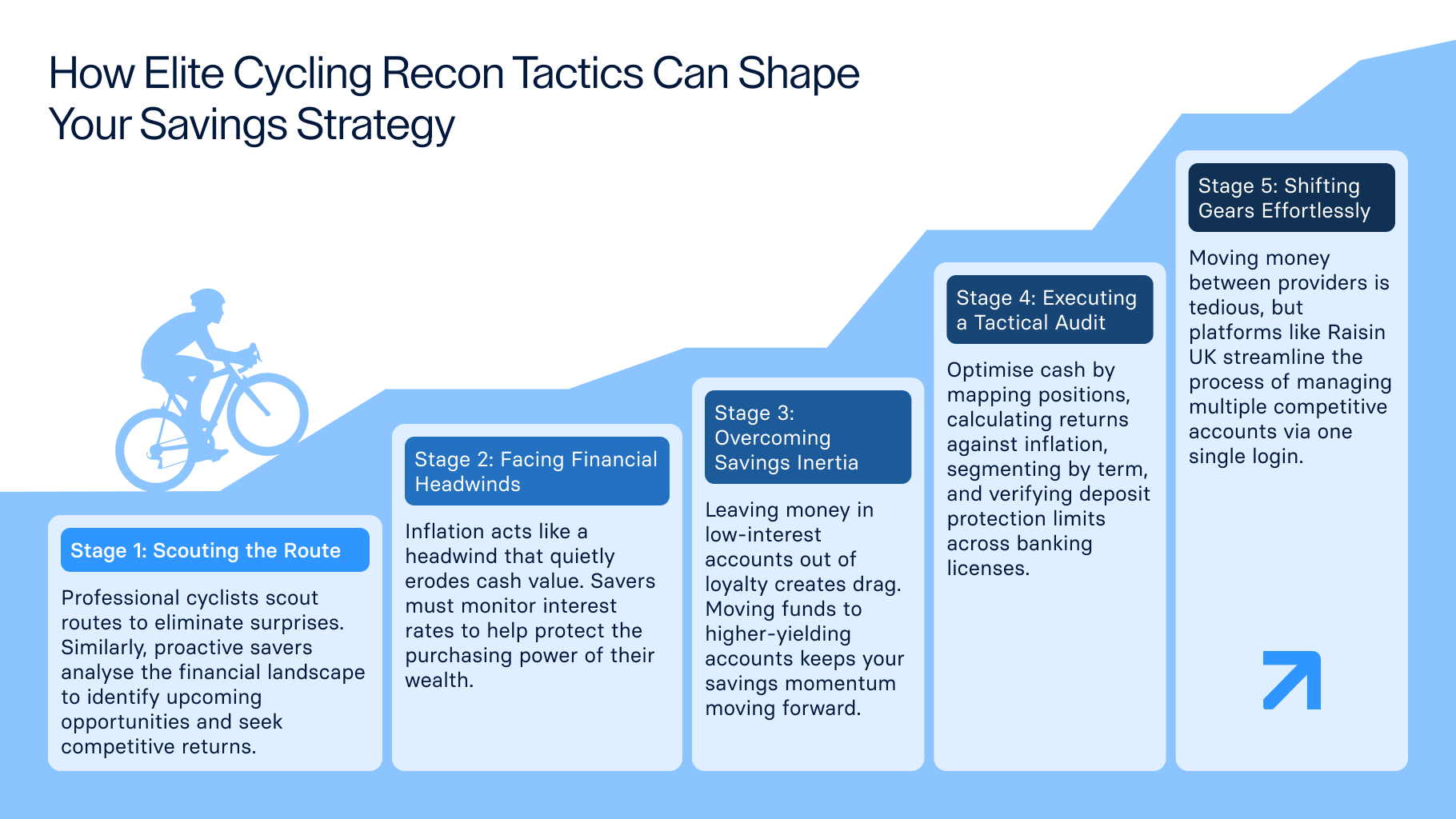

Scouting the Route

Before professional cyclists reach the starting line, they (and their team) complete a "recon" run. They study the course weeks in advance, analysing terrain and other factors to eliminate guesswork and reduce the chance of surprises on race day.

In particular, they focus on:

- Road conditions: Assessing how smooth the surface is to ensure the bikes roll as efficiently as possible.

- Wind patterns: Observing how crosswinds across open spaces might affect the group's pace.

- Bends and descents: Practising sharp corners to find the smoothest line and note any uneven ground.

Riders and teams dedicate significant resources to this preparation because they know that raw power alone is not enough to win. Even a rider in peak physical condition will struggle if their equipment isn’t tailored to the terrain, or if they misjudge the wind.

In a sport where international races can be decided by fractions of a second, eliminating unnecessary resistance is essential for success.

How does this apply to your savings? Well, just like a race course, the financial landscape is full of unknowns and variables. Where you save your money, which provider you use and wider economic factors can all affect how much return you receive on your hard-earned money. Taking a proactive approach can help you identify upcoming headwinds and tactical opportunities to make your money work that little bit harder.

Route planning with Raisin

We believe managing your savings should be as frictionless as a perfectly executed descent. That is why we let you scout the route before you even begin. You can see exactly what it takes to get started

Here is what your route looks like:

- Register for a free Raisin Account: It takes just a few minutes to provide your details.

- Choose your account and fund it: Browse competitive rates, select the offer that suits your goals, and transfer your funds.

We smooth out the road ahead by bringing savings accounts from our partner banks under a single login, helping you to avoid multiple registrations and navigate changing conditions so you can focus on your financial goals.

Navigating the Headwinds: Inflation and Interest Rates

Inflation is one of the strongest financial headwinds savers face. It exerts a steady downward pressure on your cash, quietly eroding its value over time. If inflation outpaces your rate of return, your actual wealth may diminish despite your balance rising.

Keeping up to date with inflation and comparing it to your rate of return may help your savings retain more of their value of time. Following market updates, even if it's just checking the news every now and again, can also take some of the guesswork out of your next move, giving you the clarity to make informed decisions about your money.

Inertia: Looking Beyond Loyalty

Inertia dictates that a resting object wants to remain at rest, while an object in motion will stay in motion (unless an external force restricts it). In simple terms, something that is moving will continue moving until something else stops it. Equally, something static won’t move unless encouraged.

For cyclists and their teams, working with inertia is a key factor in their overall performance. Calculating where a rider can maintain motion, or where they may require more support to build momentum, can help teams plan accordingly to ensure a smooth and optimal ride.

For savers, inertia often surfaces by leaving your money in a low interest savings account out of laziness or loyalty. While your money may grow in numerical terms, the forces of inflation may mean it loses real value over time. Moving to another account with a higher interest rate could help your money get back into motion and increase its growth potential.

Reviewing where your money sits on a regular basis can help reduce the ‘drag’ on the growth of your savings. Comparing your current rate with the wider market helps you see how easily you could secure a better return. Some savers benefit from spreading their money across multiple terms, which you can easily do at Raisin UK, or by using different types of accounts depending on their savings goals.

The Tactical Savings Audit: Optimising Your Cash Strategy

Just like a cycling team using data to optimise performance, regularly reviewing your savings can help your money work harder. While everyone’s review will differ based on their circumstances, there are four common steps that can help you to get started.

- Map your current positions: Gather clear data on your money. Where does your money sit, and how much is it earning? You may want to check the fine print on any introductory bonus rates you previously redeemed, as these accounts can drop to a lower variable rate after the initial promotional period.

- Calculate your return: Compare your current interest rates against the rate of inflation. If inflation is outpacing your interest, calculating this gap can give you a clearer view of how your purchasing power is shifting over time, allowing you to make more informed decisions.

- Segment by timeline: Review your upcoming cash needs over the short to medium term. You may want to keep money for day-to-day expenses and emergencies in an easy access savings account, while money you won’t need in the short-term may be better placed in a fixed rate bond or notice account.

- Verify your protection limits: Eligible deposits are protected by the Financial Services Compensation Scheme (FSCS) up to £120,000 per person, but this limit applies per banking license. Checking that your money falls under the FSCS umbrella can help provide more reassurance in the long-term.

Shifting Gears

Once your review is complete, you could consider moving your money into accounts with more competitive returns. However, this process can be time-consuming, especially if you open accounts across multiple providers. You may need to navigate separate registration forms, carry out multiple identity checks and manage multiple logins.

That’s where Raisin UK comes in. You can manage all of your savings in a single, streamlined platform. We give you access to FSCS-protected savings accounts from over 40 banks and building societies, helping you to earn competitive returns while benefiting from the ease of managing your money with a single login and an intuitive dashboard.

The information provided here is for informational and educational purposes only and does not constitute financial advice. Please consult with a licensed financial adviser or professional before making any financial decisions. Your financial situation is unique, and the information provided may not be suitable for your specific circumstances. We are not liable for any financial decisions or actions you take based on this information.

Save smarter with the Raisin UK newsletter!

What’s in it for me?

Receive updates on the latest interest rates

Ensure you never miss a bonus offer

Keep your finger on the pulse with the latest financial news

About us

Savings accounts

Guides

About us

Savings accounts

Guides

All interest rates displayed are Annual Equivalent Rates (AER), unless otherwise explicitly indicated. The AER illustrates what the interest rate would be if interest was paid and compounded once a year. This allows individuals to compare more easily what return they can expect from their savings over time.

Raisin UK is a trading name of Raisin Platforms Limited which is authorised and regulated by the Financial Conduct Authority (FRNs 813894 and 978619). Raisin Platforms Limited is registered in England and Wales, No 11075085. Registered office: Cobden House, 12-16 Mosley Street, Manchester M2 3AQ, United Kingdom. The information on this website does not constitute financial advice, always do your own research to ensure it's right for your specific circumstances. Tax treatment depends on the individual circumstances of each customer and may be subject to change in the future.