Accessibility and higher rates: Why a money market account makes sense for your savings

Key takeaways

A money market account (MMA) is a bank deposit account that typically offers higher interest rates than traditional savings accounts while still allowing limited withdrawals and transactions.

Money market accounts are usually FDIC-insured (or NCUA-insured at credit unions) up to applicable limits, making them a low-risk option for holding cash.

With competitive rates but some access restrictions and potential minimum balance requirements, MMAs can be a good fit for emergency funds or savings you may need in the near future.

When choosing an account to park your hard-earned money, the decision often comes down to greater accessibility or earning a higher interest rate. But a money market account (MMA), also called a money market deposit account (MMDA), may strike just the right balance between both benefits.

Here’s everything you should know before opening an MMA, and how it can factor into your savings strategy.

What is a money market account?

A money market account is a type of interest-earning savings account offered by some banks, credit unions, and online financial institutions. MMAs provide many of the conveniences of a typical savings account but with a major added benefit — they often offer higher rates than traditional or even high-yield savings accounts (HYSA).

Money market account interest rates can be similar or just slightly less than those offered through certificates of deposit (CD), but MMAs are much more liquid; CDs require you to hold a set amount of savings untouched in an account to obtain their higher rates, but with MMAs, you can withdraw and deposit money at any time without penalty fees.

Can I withdraw money from a money market account?

Withdrawals from MMAs had been limited to six per month, but in April 2020 the Federal Reserve Board announced a new regulation allowing financial institutions to lift the cap on withdrawals on all savings accounts. This announcement was introduced due to the Covid-19 pandemic to make it easier for customers to access their savings in a time of financial need.

A few months after the initial announcement, the Fed updated its Frequently Asked Questions on savings deposits to indicate that the Board does not have plans to re-impose transfer limits.

Today's top rates on Raisin

Bank

Product

APY

Maturity

mph.bank, a division of Liberty Savings Bank, F.S.B., Member FDIC

Member FDIC

Callable CD

4.00%

60 months

$2,000.00

Raisin is not an FDIC-insured bank or NCUA-insured credit union and does not hold any customer funds. FDIC deposit insurance covers the failure of an insured bank and NCUA deposit insurance coverage covers the failure of an insured credit union.

What can a money market account be used for?

A money market account allows you to earn more interest on your savings while still having easy access to your funds when needed.

These features make MMAs great options for the following savings goals:

- An emergency fund for unexpected costs, such as medical bills or car repairs

- Major expenses, like a down payment for a new home or college tuition

- Short-term wants and needs, like an upcoming vacation or new car purchase

- Extra funds that you don’t need access to on a daily basis

What to look for in a money market account

Not all money market accounts are created equal. If you’re thinking of opening an MMA, here are several factors to consider.

APY: Annual percentage yield (APY) is one of the most important figures associated with a savings account because it dictates how much you’ll earn in interest on your money. The higher the rate, the more you’ll make over time. (Learn how to calculate interest earned based on APY here.)

Unlike that of a CD, an MMA’s interest rate is variable; it may change based on overall market conditions. For example, if the Federal Reserve raises interest rates, then the rates banks offer on MMAs may increase as well. The reverse also is true.

Minimum deposit: Different MMAs have different rules for the minimum amount required to open an account — varying from as little as $1 to as high as several thousand dollars.

Minimum balance: If an MMA requires you to maintain a minimum balance — say, $1,000 — you may incur a fee if the amount in your account dips below that threshold. So, if you’d rather be able to access all of your money, be sure to look for an account that requires a low or no minimum balance.

Fees (or lack thereof): Some financial institutions charge monthly maintenance fees, which can quickly eat into your savings. Make sure you understand any fees that are associated with an account — or choose one that doesn’t charge any.

Withdrawal limits: MMAs are considered liquid, which means you can withdraw or transfer funds when needed, without penalty. Just keep in mind, some financial institutions may restrict your withdrawals to the six-per-month limit, despite recent changes in Fed rules.

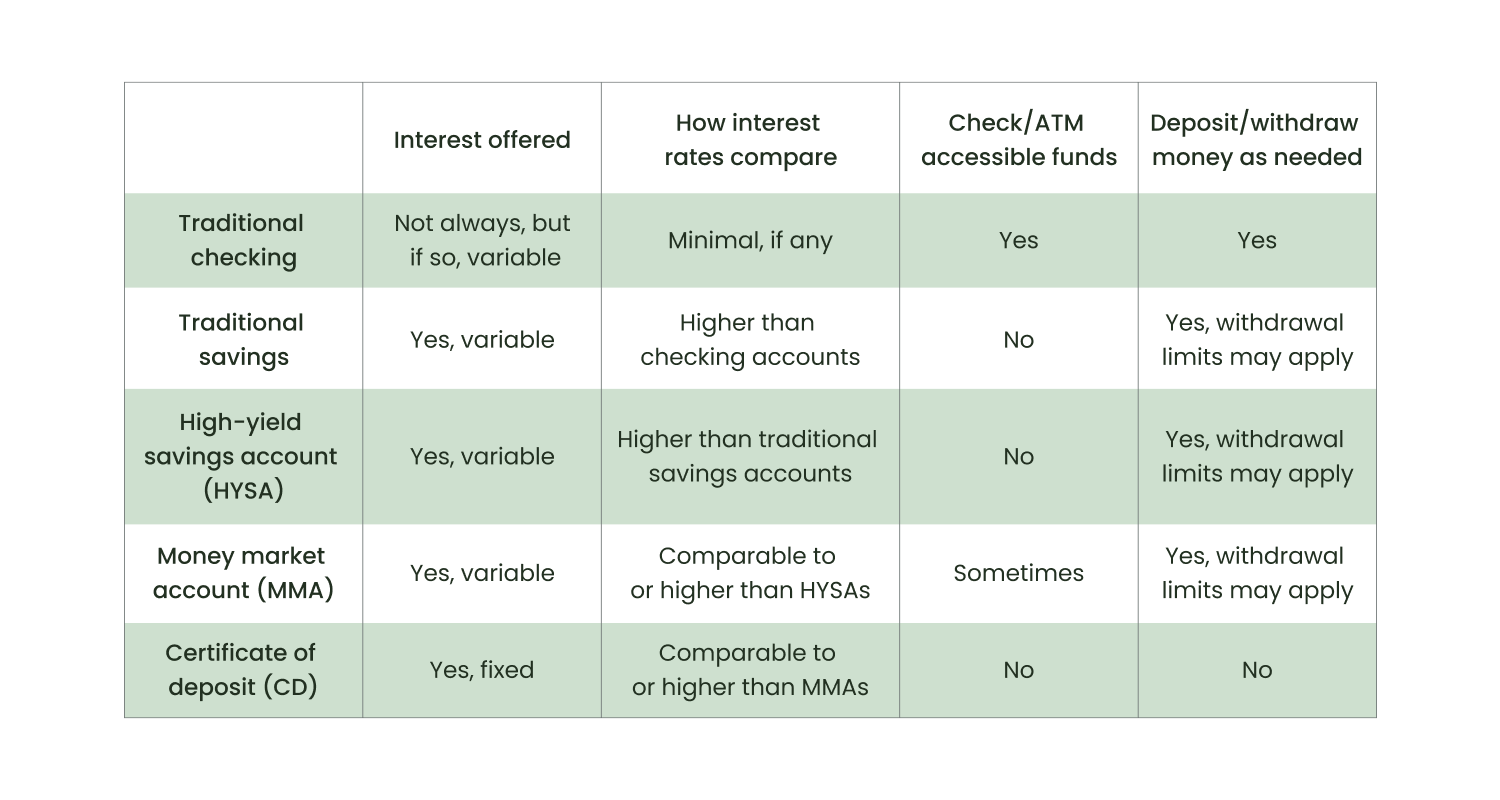

Money market accounts versus other deposit accounts

The table below compares common features found in money market accounts and other types of deposit accounts.

Luckily, you can have MMAs and other deposit accounts at the same time. This allows you to spread your savings among multiple accounts depending on your needs.

Explore your saving options with Raisin

Raisin gives you the freedom to browse and select high-yield savings products — including MMAs, HYSAs, and CDs — through one easy-to-use platform. Our exclusive network of banks and financial institutions offers high-yield savings products that can be opened with an initial deposit of just $1. Plus, there are no fees charged for MMAs available through Raisin, and there are currently no limits on withdrawals.

Ready to get started with high-yield accounts that meet all your needs? Find out how Raisin streamlines the process, making saving for your future easier than ever before.

The above article is intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law, or any other business and professional matters that affect you and/or your business.

© 2026 Raisin SE. All rights reserved.

The Raisin name and logo are trademarks of Raisin SE. All other trademarks, logos, marks, and brand names are the property of their respective owners.

*APY means Annual Percentage Yield. APY is accurate as of April 17, 2026. Interest rate and APY may change after initial deposit depending on the terms of the specific product selected. Minimum opening deposit is $1.00.

Raisin is not an FDIC-insured bank, and FDIC deposit insurance only covers the failure of an insured bank.

Raisin is not an NCUA-insured credit union. NCUA deposit insurance only covers the failure of an insured credit union.

Raisin does not hold any customer funds. Customer funds are held in various custodial deposit accounts. Each customer authorizes the Custodial Bank to hold the customer’s funds in such accounts, in a custodial capacity, in order to effectuate the customer’s deposits to and withdrawals from the various bank and credit union products that the customer requests through Raisin.com. The Custodial Bank does not establish the terms of the bank or credit union products and provides no advice to customers about bank or credit union products offered by the applicable bank or credit union through Raisin.com. Each customer also authorizes the Service Bank to move funds among the various banks and credit unions at the customer’s request. First International Bank & Trust (FIBT), Member FDIC, is the Service Bank. Bell Bank and Starion Bank, each Member FDIC, are the Custodial Banks.

†Based on $250,000 in FDIC or NCUA insurance coverage per insurable category of ownership at each partner bank or credit union on the Raisin platform (each a "Product Bank"), when aggregated with all other deposits held by you at such Product Bank and in the same insurable category. Deposits made through Raisin will be eligible to receive deposit insurance from the FDIC or the NCUA (each a "Deposit Insurer") in accordance with and up to the maximum amount permitted by law at each Product Bank. Raisin is not a bank or credit union and does not hold any customer funds. Funds are held at FDIC-insured banks and NCUA-insured credit unions. Deposit insurance covers the failure of an insured bank or credit union. Certain conditions must be satisfied for pass through deposit insurance coverage to apply. Customers may choose to deposit funds with identically registered accounts at different Product Banks on the Raisin platform to be eligible for Deposit Insurer coverage up to $10 million for individual accounts and $20 million for joint accounts when at least 40 Product Banks are utilized. Please be aware, however, that any deposits you have at a Product Bank, whether through the Raisin platform or outside the Raisin platform, that you may hold in the same capacity (such as in an individual capacity or joint capacity) count toward the applicable Deposit Insurer's deposit insurance maximum amount, and any such amounts that you hold in the same capacity at a Product Bank that exceed the maximum insurance coverage by the applicable Deposit Insurer will not be insured. For more information on FDIC deposit insurance, please see here. For more information on the NCUA share insurance fund, please see here. You are solely responsible for monitoring the amount of funds you have on deposit at each a Product Bank, whether through the Raisin platform or outside the Raisin platform, to confirm that the deposits you hold in the same capacity at each Product Bank do not exceed the maximum deposit insurance coverage provided by the applicable Deposit Insurer.