Financially frazzled: How do age, gender and location affect savings in the United States?

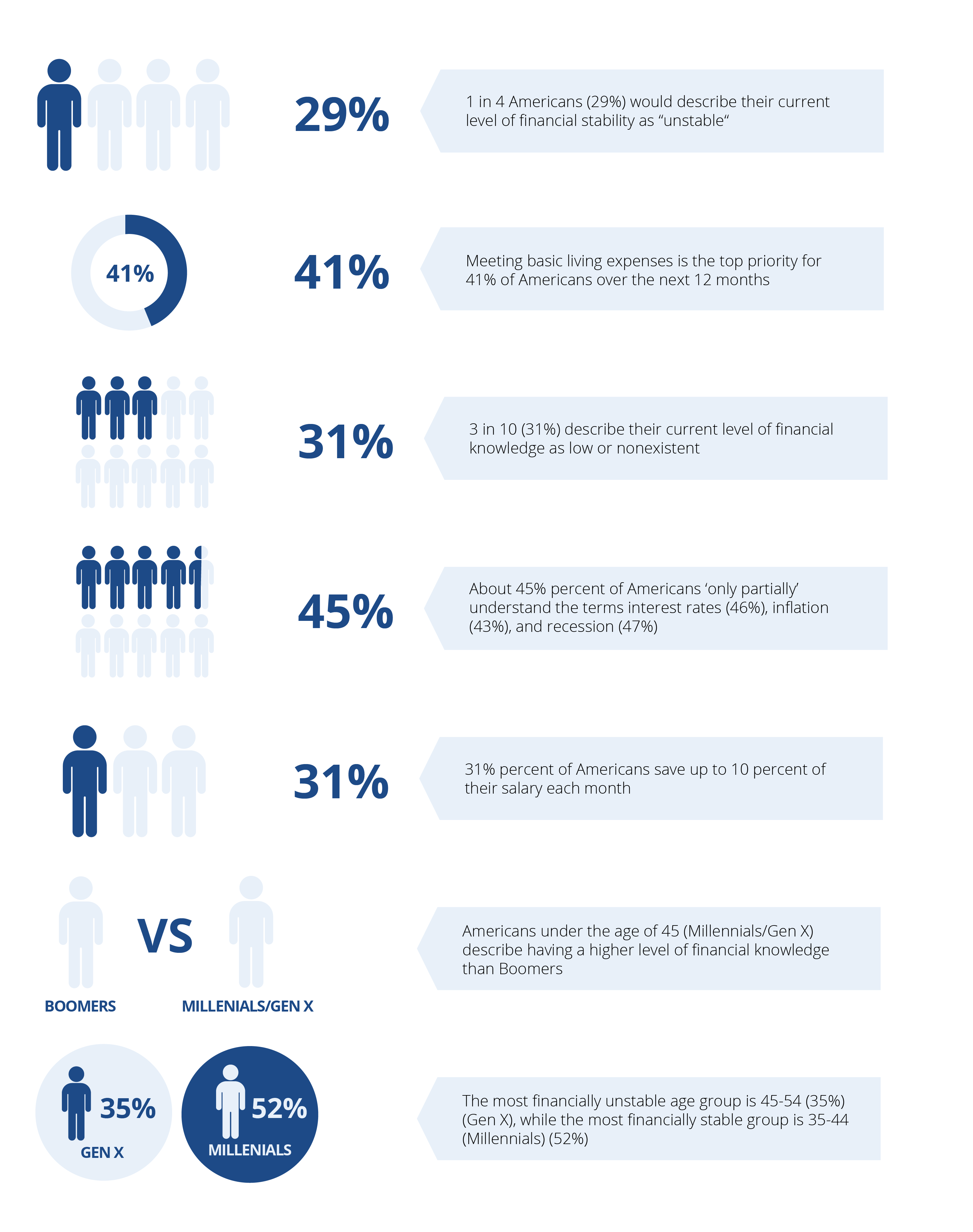

Inflation, interest, and recession are all words we hear on a daily basis, but how many Americans know what these money terms mean and, more importantly, the impact they have on the dollars in your pocket? Research has found that 17 million Americans would say they have “no financial knowledge,” which could be impacting their ability to plot their own finances, with 3 in 10 (31%) describing their level of financial knowledge as low or non-existent. We surveyed 4,000 adults across 21 cities in the US to find out how Americans are managing their finances in 2023.

Which city has the best savers?

As households continuously review budgets and admit to growing pressure from the cost of living, the data signaled a worrying statistic: 1 in 4 (29%) of people in the US describe their current financial situation as “unstable,” with San Diego (40%) and Denver (36%) topping the list.

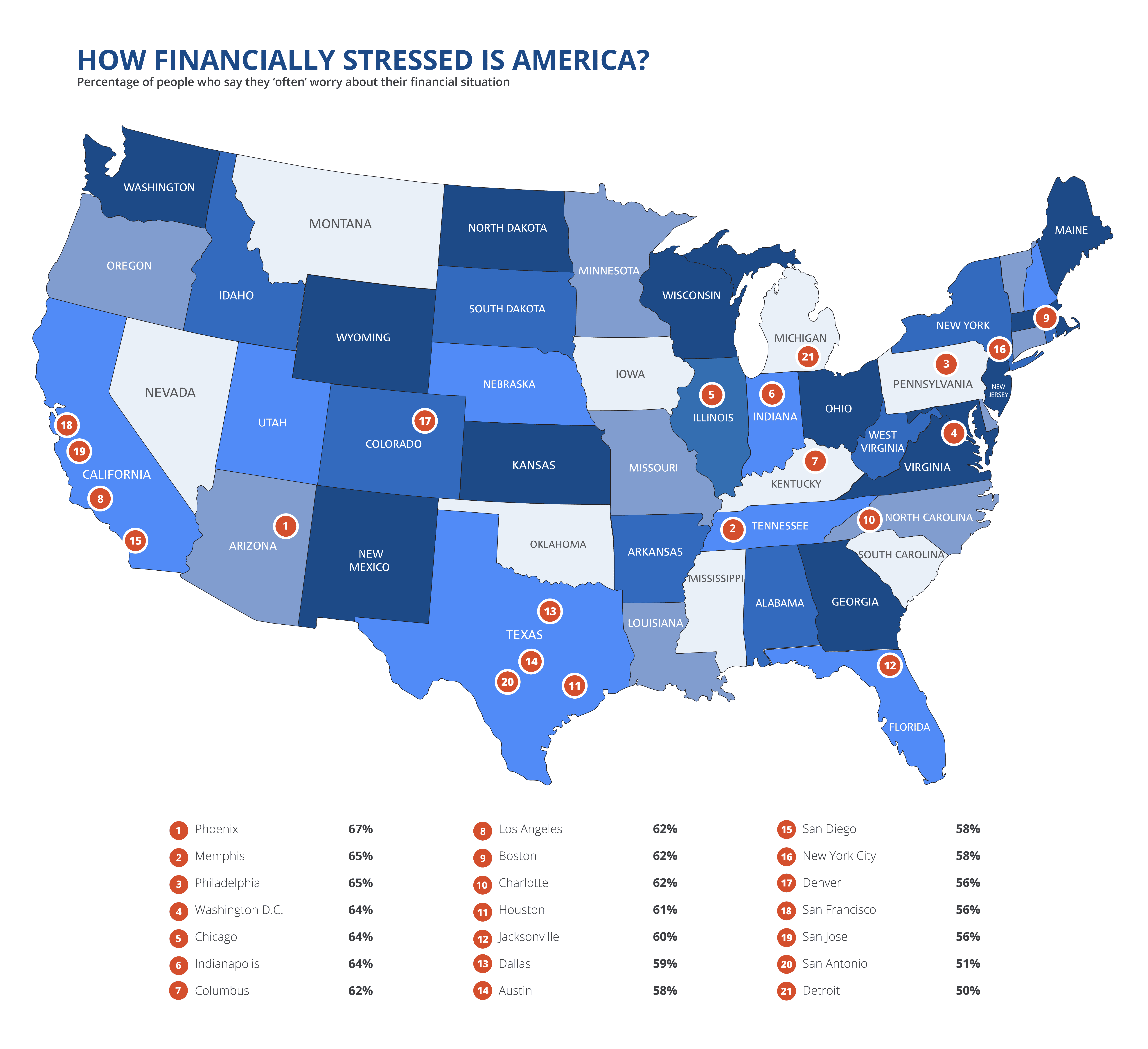

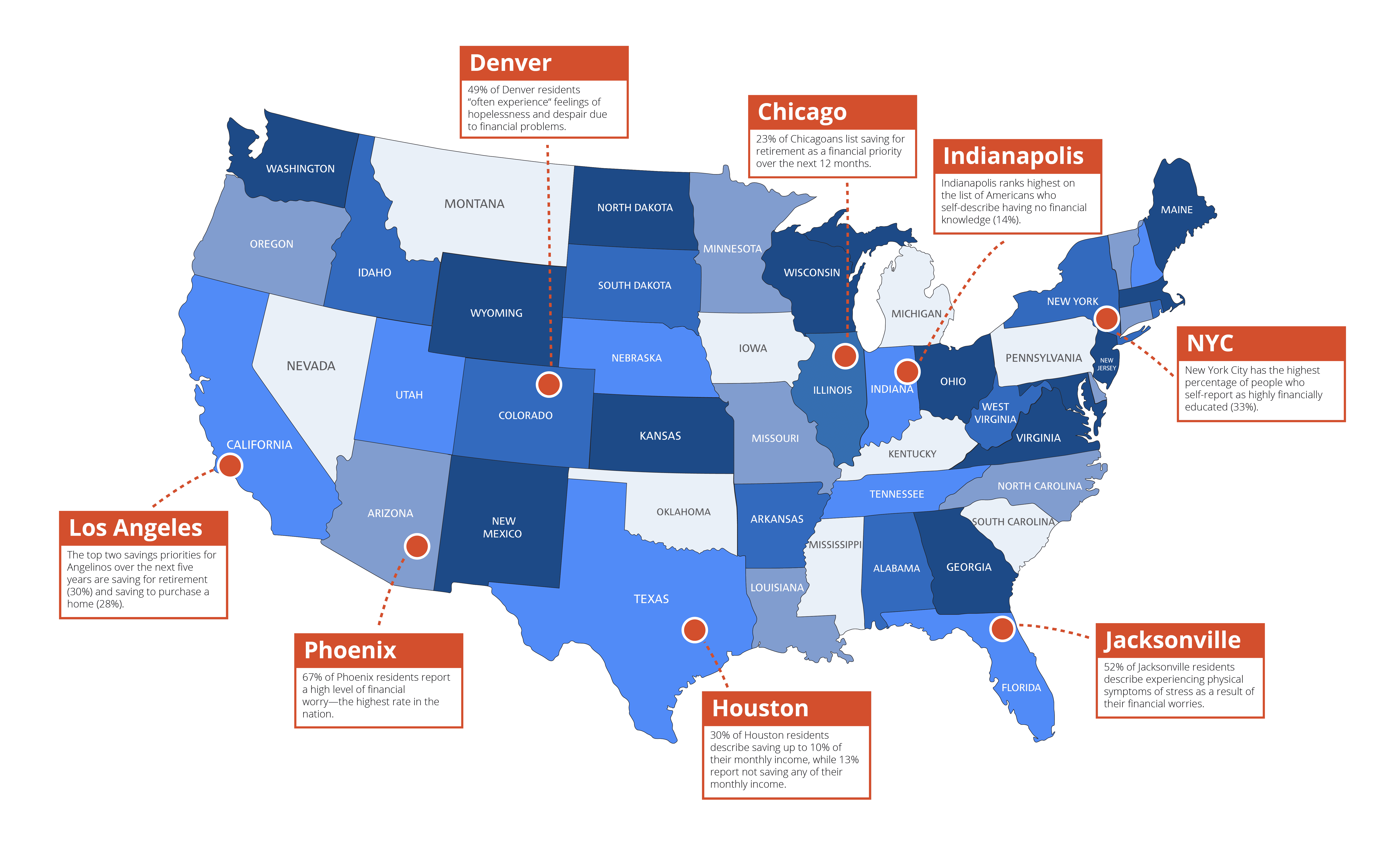

Money is an emotionally harrowing topic for American adults, as half (50%) of Americans often experience feelings of hopelessness and despair due to financial difficulties. San Francisco reports the lowest level of financial worry: 28% of people here do not worry often about their finances, compared to a whopping 67% of people living in Phoenix, while Columbus residents are more likely to experience physical symptoms resulting from financial stress, such as headaches, than in any other city in the US (56%). Phoenix and Columbus also rank high for percentages of adults that anticipate cutting costs this year, at 63% and 56% respectively, joining cities like Memphis (62%) and Indianapolis (60%).

So what are people doing to improve their financial situation? For 1 in 2 Americans (50%), the answer was simple: cutting costs. Taking out a loan was among preferred options in Los Angeles (13%), while San Diego reported the highest number of people who answered that they were investing in stocks and funds (30%), followed closely by New York (29%) and Los Angeles (28%). Americans in Boston and Chicago are less likely than people in Houston or San Jose to ask friends and family to borrow money (12% and 11%, compared to 19% and 20%) in order to improve their financial situation.

Regarding financial literacy, Denver has the highest number of people who report having “low or no financial knowledge” (39%); while in Austin and New York City, three-quarters (76%) of people describe themselves as having a mid or high level of financial knowledge.

New data also highlights priorities for people in the US when it comes to financial planning, with 16% of Americans responding that they never save any of their monthly income. Our survey showed that the North East is home to some of the best savers in the US – with 79% saving money every single month. In terms of what people are saving for, we found that San Fransiscans are the most likely to be saving for retirement (27%), followed by Bostonians (24%). People in Memphis (21%), Detroit (22%), and Philadelphia (22%) are the least likely to prioritize buying a house within the next five years.

Battle of the sexes

Nearly two thirds (65%) of women say they often worry about finances, with 57% of men agreeing with this sentiment. Overall, men tend to be more optimistic about improving their financial situation, with 63% of respondents saying they feel optimistic or very optimistic, compared to 52% of women. We found that nearly 1 in 4 men (24%) described their financial situation as “unstable,” compared to 33% of women.

And while over half (56%) of women say they will cut costs in order to improve their financial situation, only 44% of men agree. Instead, men are more likely to opt for savings and investment products, including fixed rate deposits (24% vs 19%), investing in stocks (26% vs 15%) and investing in crypto (17% vs 6%).

When it comes to financial planning, 41% of Americans respond that their top priority for the next 12 months is simply meeting basic living expenses. The next ranking priorities for men are paying off debt and saving for emergencies (30% each). The second ranked priority for women is also paying off debt, at 41%.

The age factor

It’s not necessarily the younger generations who live with the highest level of financial instability: we found that while 1 in 4 Americans aged 18-24 (27%) described their current financial situation as “unstable,” this figure was higher amongst all other age groups, with 45-54 year olds ranking highest (35%), followed by ages 55+ (29%).

Just over two thirds (68%) of 35-44 year olds say they often worry about finances, the highest of any age group. Generally, younger people tend to be more optimistic about their finances, with roughly 60% of those under 44 reporting they feel optimistic about improving their situation in the next six months, compared to less than 52% of those 45-54, and 47% of Americans over 55.

The 55+ age group is most likely to cut costs in order to improve their financial situation (60%), although this is the preferred method reported by all age groups.

Meeting basic living expenses was the number one priority across the board, while the second biggest priority for the next 12 months for 18-24 year olds is saving for a car (34%).

The Raisin view

Discussing the findings, Cetin Duransoy, CEO of Raisin US, highlighted: “A significant number of people are struggling to make proactive financial decisions. This is evident across different age groups and income levels, from those who find it challenging to set aside money for emergencies to retirees who struggle to make their retirement savings work during the current economic crisis. No matter what your personal circumstances may be, understanding how to make informed financial decisions is crucial.

“Our new ‘Journey to Financial Wellness’ initiative seeks to assist consumers in improving their financial literacy and making more informed financial decisions in just half an hour. This campaign aims to address people’s challenges in managing their finances by providing them with easy-to-understand information and guidance.”

Methodology

Raisin surveyed 4,000 adults from 21 American cities on 7/21/2023. More information available on request.

Is there anything else I need to know?

Getting started with Raisin is simple and — best of all — there are no fees! We’re here to help you get the most out of your savings journey and have lots of resources to help you better understand Raisin and your finances. Take a look below for some help on the basics of signing up for an account to figuring out how to create the best savings strategy possible.

How Raisin works

Find out more how Raisin works and how funds move through our platform.

Education Center

Learn more with savings tips and guides on how to get the most out of Raisin.

How to register

This step-by-step guide will show you exactly how to open a Raisin account.

© 2026 Raisin SE. All rights reserved.

The Raisin name and logo are trademarks of Raisin SE. All other trademarks, logos, marks, and brand names are the property of their respective owners.

*APY means Annual Percentage Yield. APY is accurate as of August 7, 2026. Interest rate and APY may change after initial deposit depending on the terms of the specific product selected. Minimum opening deposit is $1.00.

Raisin is not an FDIC-insured bank, and FDIC deposit insurance only covers the failure of an insured bank.

Raisin is not an NCUA-insured credit union. NCUA deposit insurance only covers the failure of an insured credit union.

Raisin does not hold any customer funds. Customer funds are held in various custodial deposit accounts. Each customer authorizes the Custodial Bank to hold the customer’s funds in such accounts, in a custodial capacity, in order to effectuate the customer’s deposits to and withdrawals from the various bank and credit union products that the customer requests through Raisin.com. The Custodial Bank does not establish the terms of the bank or credit union products and provides no advice to customers about bank or credit union products offered by the applicable bank or credit union through Raisin.com. Each customer also authorizes the Service Bank to move funds among the various banks and credit unions at the customer’s request. First International Bank & Trust (FIBT), Member FDIC, is the Service Bank. Bell Bank and Starion Bank, each Member FDIC, are the Custodial Banks.

†Based on $250,000 in FDIC or NCUA insurance coverage per insurable category of ownership at each partner bank or credit union on the Raisin platform (each a "Product Bank"), when aggregated with all other deposits held by you at such Product Bank and in the same insurable category. Deposits made through Raisin will be eligible to receive deposit insurance from the FDIC or the NCUA (each a "Deposit Insurer") in accordance with and up to the maximum amount permitted by law at each Product Bank. Raisin is not a bank or credit union and does not hold any customer funds. Funds are held at FDIC-insured banks and NCUA-insured credit unions. Deposit insurance covers the failure of an insured bank or credit union. Certain conditions must be satisfied for pass through deposit insurance coverage to apply. Customers may choose to deposit funds with identically registered accounts at different Product Banks on the Raisin platform to be eligible for Deposit Insurer coverage up to $10 million for individual accounts and $20 million for joint accounts when at least 40 Product Banks are utilized. Please be aware, however, that any deposits you have at a Product Bank, whether through the Raisin platform or outside the Raisin platform, that you may hold in the same capacity (such as in an individual capacity or joint capacity) count toward the applicable Deposit Insurer's deposit insurance maximum amount, and any such amounts that you hold in the same capacity at a Product Bank that exceed the maximum insurance coverage by the applicable Deposit Insurer will not be insured. For more information on FDIC deposit insurance, please see here. For more information on the NCUA share insurance fund, please see here. You are solely responsible for monitoring the amount of funds you have on deposit at each a Product Bank, whether through the Raisin platform or outside the Raisin platform, to confirm that the deposits you hold in the same capacity at each Product Bank do not exceed the maximum deposit insurance coverage provided by the applicable Deposit Insurer.