Banca Più

2.96 %AER

All you need to know about European Central Bank rates

The European Central Bank (ECB) plays a crucial role in determining key interest rates that influence the economy of the Eurozone – including Ireland. This guide explains how the ECB sets these rates, what the different types of rates are (such as deposit and lending rates), and how they affect savings and borrowing.

The European Central Bank manages the monetary policy of the Eurozone, which includes Ireland

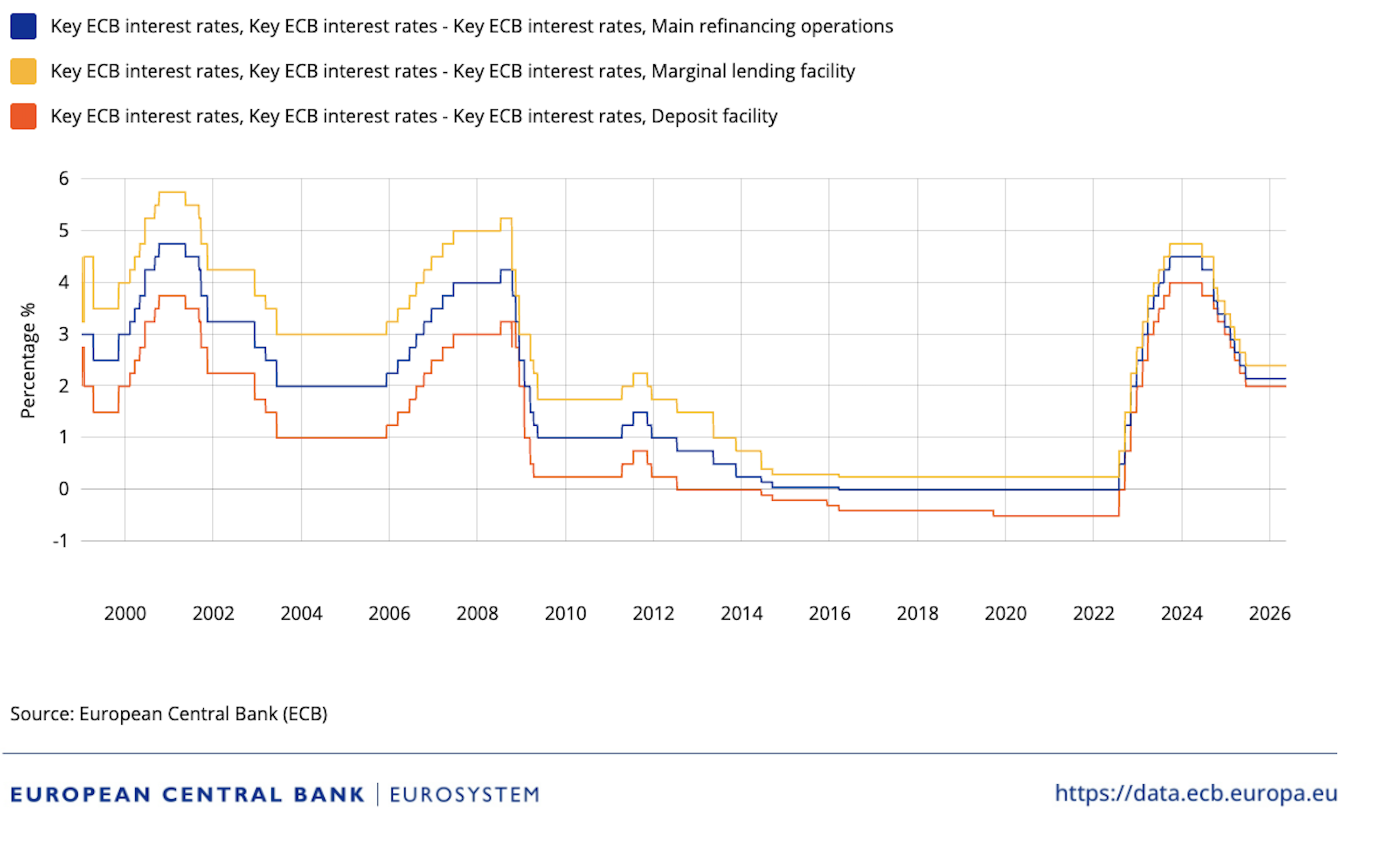

The ECB sets three key interest rates, which have different purposes within the banking system

The rate set by the ECB can affect what you pay on mortgages or loans and what you earn on savings

The information provided here is for informational and educational purposes only and does not constitute financial advice. Please consult with a licensed financial adviser or professional before making any financial decisions. Your financial situation is unique, and the information provided may not be suitable for your specific circumstances. We are not liable for any financial decisions or actions you take based on this information.

The latest decision was made on 23 July 2026, with the ECB holding the three key interest rates steady:

The main refinancing rate is 2.40%

The marginal lending rate is 2.65%

The deposit rate is 2.25%

The ECB’s governing council meets every six weeks to set these interest rates for the euro area. To find the most up-to-date rates, you can check the ECB website.

A few trends can be seen from the chart: sharp cuts following the 2008 financial crisis, a long period of very low rates, and then the more recent series of increases as the ECB worked to bring inflation back under control.

The ECB sets three key interest rates that serve different purposes in the banking system and the Eurozone economy as a whole:

Main refinancing rate (or main refinancing operations): The interest rate banks pay when they borrow money from the ECB for one week.

Deposit interest rate (or deposit facility): The interest rate the ECB pays (or charges) on overnight deposits that banks hold with the ECB or other national central banks in the euro area (the Eurosystem).

The main refinancing rate is the interest rate banks pay when they borrow funds from the ECB for a short period, usually one week. This rate influences the overall level of interest rates on borrowing in the euro area, affecting everything from business loans to mortgages. By adjusting this rate, the ECB can influence the amount of money in circulation, aiming to either stimulate economic activity or slow down inflation.

The deposit rate is the interest rate banks receive (or pay, if rates are negative) when they deposit funds overnight with the ECB or national central banks in the Eurosystem. A negative deposit rate means that banks are charged for keeping their money with the ECB, encouraging them to lend more to businesses and consumers. Conversely, a higher deposit rate makes it more attractive for banks to hold money with the central bank. Banks may then increase the interest rates they offer on savings accounts to stay competitive.

The marginal lending rate is the rate at which banks can borrow additional funds from the ECB overnight using eligible collateral, often as a last resort. This rate is typically higher than the main refinancing rate, as it serves as a penalty rate for banks that need emergency liquidity. Its existence therefore ensures that banks have access to funds, while discouraging excessive reliance on ECB support.

The ECB’s primary objective is to maintain price stability and preserve the purchasing power of the euro. To do this, it aims to keep inflation – the rate at which the prices for goods and services change over time – low, stable, and predictable. The ECB believes that a moderate level of inflation of around 2% provides the conditions for steady economic growth. This is the same as the target set in the UK and the United States.

The ECB rate may affect your mortgage if you have a variable-rate mortgage. When the ECB raises rates, the cost of borrowing typically increases, leading to higher mortgage payments. Conversely, if the ECB lowers rates, your mortgage payments may decrease.

In Ireland, tracker mortgages are directly linked to the ECB rate, so these changes usually lead to immediate adjustments in monthly payments. The exact impact depends on your mortgage agreement and how closely your lender's rates track the ECB's rates.

ECB interest rates also influence the interest rates offered on savings accounts. When rates rise, savers might earn more on their deposits.

Regardless of what happens with the ECB rates next, it can be a useful prompt to review your savings strategy. Whether you want to take advantage of current interest rates or build a financial buffer, opening a savings account can help you manage your money effectively.

To compare interest rates on savings accounts, register for a Raisin Account and log in to apply.

ECB stands for European Central Bank. This is the central bank responsible for managing the monetary policy of the Eurozone, which comprises Ireland and 19 other EU member states that use the euro. The ECB’s primary mission is to maintain price stability within the Eurozone by controlling inflation and ensuring the smooth operation of the financial system.

When people talk about ECB rates, they are referring to the interest rates set by the European Central Bank. These rates influence the cost of borrowing money, the return on savings, and overall economic activity in the euro area. By increasing or decreasing these rates, the ECB can either encourage or discourage spending and investment, in order to keep inflation in check and support economic growth.

The ECB uses three key interest rates: the deposit facility rate, the main refinancing rate, and the marginal lending rate. Among these, the deposit facility rate has been described by the ECB’s governing council as the rate “through which we steer the monetary policy stance.” Meanwhile, the main refinancing rate remains crucial as a weekly benchmark for bank borrowing in the euro area. So no single rate is more important than the other; each one plays a role in Europe’s monetary policy.

The ECB exchange rate refers to the official exchange rates published by the European Central Bank, reflecting the value of the euro against other currencies. These rates are used as reference rates for transactions and financial reporting and are updated regularly based on prevailing market conditions.

The ECB affects financial markets in Ireland and across the euro area in several ways. Changes to ECB rates can influence everything from stock prices to bond yields to the value of the euro. Banks may adjust rates on their products (for example, mortgages, savings accounts, and loans) in response to an ECB rate cut or hike. A rate hike might strengthen the euro as higher interest rates can attract foreign investment, while a rate cut could boost stock markets by lowering borrowing costs for companies.

Following the most recent ECB decision in July, Jasmin Ehlert, Head of Bank Analytics at Raisin, noted that:

"It is expected that the central bank will resume rate hikes in September — especially given the conflict in the Middle East and high energy prices.

For savers, this means you can continue to enjoy high interest rates. Short-term fixed deposit accounts and competitive demand deposit accounts can be useful ways to bridge the gap until the next decision in the autumn. By then, you might benefit from even higher rates."

© 2026 Raisin Bank AG, Frankfurt a.M.

All interest rates displayed are Annual Equivalent Rates (AER), unless otherwise explicitly indicated. The AER illustrates what the interest rate would be if interest was paid and compounded once a year. This allows individuals to compare more easily what return they can expect from their savings over time. Raisin Bank, trading as Raisin, is authorised/licensed or registered by BaFin (Bundesanstalt für Finanzdienstleistungsaufsicht) in Germany and is regulated by the Central Bank of Ireland for conduct of business rules.

.png&w=3840&q=100)