What is investment risk tolerance and why is it important?

The key to confident investing: Assessing your risk tolerance

Key takeaways

Your risk tolerance plays a crucial role in shaping your investment strategy, influencing the balance between high-risk and low-risk assets in your portfolio.

Your age, financial goals, investment timeline, portfolio size, and comfort level with risk all contribute to how much risk you are willing and able to take.

By aligning your investments with your risk tolerance, you can reduce emotional decision-making, improve long-term resilience, and achieve financial stability while staying within your comfort zone.

Definition: What is risk tolerance?

Simply put, risk tolerance refers to the level of risk an investor is willing and able to take when making investment decisions. It plays a crucial role in shaping your investment strategy, influencing both the types and the number of investments you choose. By understanding your risk tolerance, you can effectively plan and structure your investment portfolio before committing any capital.

Investments in stocks, equity funds, or exchange-traded funds (ETFs) typically require a higher risk tolerance due to their greater volatility. On the other hand, bonds, bond funds, and income funds are generally associated with a lower risk tolerance, as they tend to offer more stability and lower potential losses.

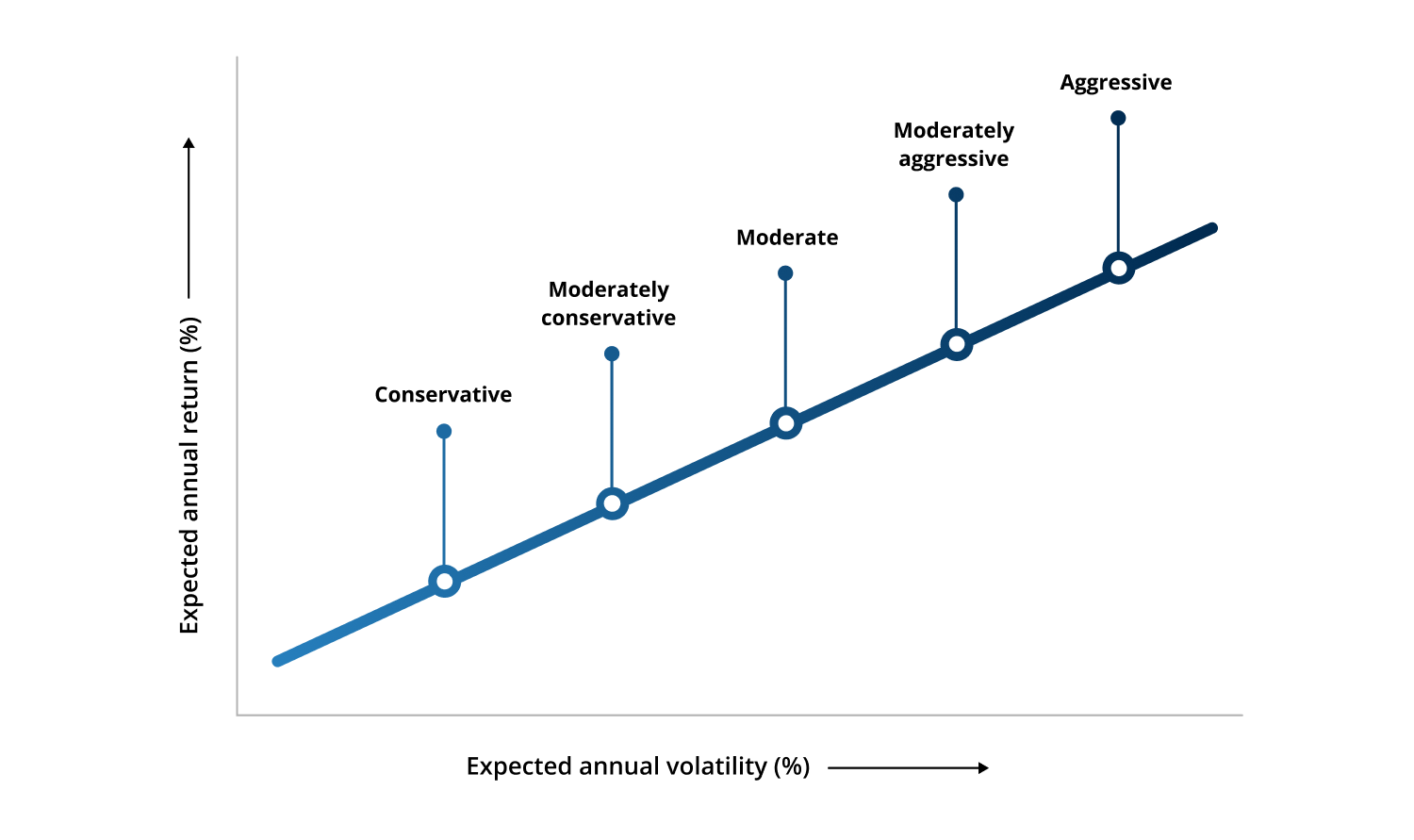

Different levels of investment risk tolerance

Usually, risk tolerance in the financial sector can be separated into three different levels or categories. Depending on how much risk an investor can tolerate when investing their money, they have either an aggressive, moderate, or conservative risk tolerance.

Aggressive risk tolerance

An aggressive risk tolerance investor takes very high risks and has the willingness to lose money in pursuit of potentially greater returns. However, they usually have extensive and versatile knowledge of the markets they invest in. Therefore, it is not unusual for aggressive risk tolerance investors to experience large upward and downward movements in their portfolio. They are often wealthy, experienced, and manage large investment portfolios.

Asset classes that are highly volatile — meaning they have dynamic price movements — are preferred by aggressive risk tolerance investors, such as equity funds. Due to the high risks they take, they often achieve outstanding returns when the market is performing well but can also face significant losses if market performance falls short of their expectations. As a result, aggressive investors don’t tend to panic sell during times of market crises, as they are accustomed to large fluctuations on a regular basis.

Moderate risk tolerance

Compared to aggressive risk investors, a moderate investor tends to be far less risk tolerant. This means they still show a willingness to take some risk, but they determine a certain percentage of acceptable loss. Investments suited for moderate risk tolerance are more balanced. Their goal is to invest money in both risky and safe asset classes.

Usually, moderate investors include a mixture of stocks and bonds in their portfolio. This means they might earn less than investors with an aggressive strategy, but they are also unlikely to experience huge losses when a market performs poorly, resulting in potentially more stable returns.

Conservative risk tolerance

If you prefer to take the least amount of risk with your investments, your risk tolerance is considered conservative. This means your goal is to invest only in assets that feel the safest, while actively avoiding risk. A conservative risk tolerance prioritizes avoiding losses over making gains. As a result, the investment options for this risk tolerance strategy are more limited. For example, certificates of deposit (CDs) and other low-risk savings products may be suitable asset classes for a conservative approach, as they typically offer capital protection and minimal risk.

Which factors influence my risk tolerance?

There are different types of risk tolerance, but what influences your risk tolerance? Several factors determine which investment strategy suits you best and what level of risk tolerance is right for you. Below are the most important factors that shape your risk tolerance.

Age

Your age influences your willingness to take risks. In investment planning, younger individuals typically find it easier to recover from losses, as they have many working years ahead. Time plays a crucial role in investing. Younger investors have more time to wait out market downturns and benefit from long-term growth, making it easier to navigate market fluctuations.

In some cases, younger investors may also have fewer financial obligations, such as mortgages or dependents, allowing them to take on higher-risk investments. While young investors can afford to take more risks, risk tolerance remains a personal factor. Not everyone is comfortable with high-risk investments, and factors like financial stability, personal goals, and emotional tolerance should also be considered.

Goals

Financial goals vary significantly from person to person. It is not everyone’s primary ambition to maximize their wealth. Financial goals shape investment strategies, as individuals prioritize different objectives such as wealth accumulation, financial security, early retirement, homeownership, or education funding.

Investment strategies are often tailored to meet specific goals rather than simply maximizing returns. Risk tolerance varies depending on these objectives. Additionally, risk tolerance is dynamic and can change over time based on financial needs and circumstances. Not everyone seeks to maximize returns at any cost. Many investors prioritize stable returns over high-risk investments, balancing risk and security to align with their long-term financial plans.

Timeline

Your timeline or time horizon is a critical factor when it comes to risk tolerance. Generally speaking, a longer time frame allows for greater risk-taking. One reason for this is that market trends show that, over the long run, markets tend to grow despite short-term volatility.

An investor with 15 years to invest can therefore take on more aggressive risk than someone with five years who has less time to recover from losses. As a consequence, it is common for investors with a short time horizon to opt for lower-risk investments.

Portfolio size

Generally, a larger portfolio provides a greater financial cushion and therefore allows for greater risk-taking and a more aggressive risk tolerance. For example, if you suffer a 10% loss on a $50 million portfolio compared to a $5 million portfolio, the drop is far less impactful on the larger portfolio.

A larger portfolio also allows for a broader asset allocation and enables investors to invest their money in alternative assets with higher returns which ultimately reduces the risk exposure. With more capital, it is also much easier to remain composed during downturns. This means the emotional pressure is lower and it’s easier to avoid panic-driven decisions.

Comfort level

Each investor perceives and handles risk differently. While some investors are naturally comfortable with uncertainty and high-risk investments, others find market volatility stressful and unsettling. Psychological factors, such as past experiences, financial security, and investment knowledge, play a significant role in shaping an investor’s risk tolerance.

On the other hand, those who struggle with market fluctuations may prefer low-risk investments to maintain peace of mind. Risk tolerance is ultimately a personal trait, directly tied to an investor’s ability to stay confident and composed while taking financial risks.

Risk tolerance meaning: Why is it important for my investment?

Understanding your risk tolerance is crucial because it helps you choose the right investment strategy, ensuring that your portfolio aligns with your financial goals, time horizon, and emotional comfort with risk. Investing without considering risk tolerance can lead to poor financial decisions, unnecessary stress, and losses that exceed your comfort level.

Here are the most important points why risk tolerance is crucial for your investments:

Helps build the right portfolio: Determines the balance between high-risk and low-risk assets, shaping your investment strategy.

Reduces emotional decision-making: Prevents panic selling during market downturns and impulsive investing in high-risk opportunities.

Aligns with your financial goals: Ensures your investment choices support short-term and long-term financial objectives, like retirement or wealth accumulation.

Improves market resilience: Helps you stay invested even during volatile market conditions, increasing your chances of long-term success.

Manages potential losses: Sets clear boundaries on how much risk you’re willing to take, preventing excessive financial setbacks.

Explore savings accounts to meet your financial needs at Raisin

Are you making the most of your savings while considering your risk tolerance? You don’t need to wait for professional advice to optimize your low-risk financial strategy. With Raisin, you can access multiple high-yield savings products and manage them easily in one place, ensuring your funds are working for you while staying within your comfort level.

The above article is intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law, or any other business and professional matters that affect you and/or your business.

Related Content

© 2026 Raisin SE. All rights reserved.

The Raisin name and logo are trademarks of Raisin SE. All other trademarks, logos, marks, and brand names are the property of their respective owners.

*APY means Annual Percentage Yield. APY is accurate as of July 26, 2026. Interest rate and APY may change after initial deposit depending on the terms of the specific product selected. Minimum opening deposit is $1.00.

Raisin is not an FDIC-insured bank, and FDIC deposit insurance only covers the failure of an insured bank.

Raisin is not an NCUA-insured credit union. NCUA deposit insurance only covers the failure of an insured credit union.

Raisin does not hold any customer funds. Customer funds are held in various custodial deposit accounts. Each customer authorizes the Custodial Bank to hold the customer’s funds in such accounts, in a custodial capacity, in order to effectuate the customer’s deposits to and withdrawals from the various bank and credit union products that the customer requests through Raisin.com. The Custodial Bank does not establish the terms of the bank or credit union products and provides no advice to customers about bank or credit union products offered by the applicable bank or credit union through Raisin.com. Each customer also authorizes the Service Bank to move funds among the various banks and credit unions at the customer’s request. First International Bank & Trust (FIBT), Member FDIC, is the Service Bank. Bell Bank and Starion Bank, each Member FDIC, are the Custodial Banks.

†Based on $250,000 in FDIC or NCUA insurance coverage per insurable category of ownership at each partner bank or credit union on the Raisin platform (each a "Product Bank"), when aggregated with all other deposits held by you at such Product Bank and in the same insurable category. Deposits made through Raisin will be eligible to receive deposit insurance from the FDIC or the NCUA (each a "Deposit Insurer") in accordance with and up to the maximum amount permitted by law at each Product Bank. Raisin is not a bank or credit union and does not hold any customer funds. Funds are held at FDIC-insured banks and NCUA-insured credit unions. Deposit insurance covers the failure of an insured bank or credit union. Certain conditions must be satisfied for pass through deposit insurance coverage to apply. Customers may choose to deposit funds with identically registered accounts at different Product Banks on the Raisin platform to be eligible for Deposit Insurer coverage up to $10 million for individual accounts and $20 million for joint accounts when at least 40 Product Banks are utilized. Please be aware, however, that any deposits you have at a Product Bank, whether through the Raisin platform or outside the Raisin platform, that you may hold in the same capacity (such as in an individual capacity or joint capacity) count toward the applicable Deposit Insurer's deposit insurance maximum amount, and any such amounts that you hold in the same capacity at a Product Bank that exceed the maximum insurance coverage by the applicable Deposit Insurer will not be insured. For more information on FDIC deposit insurance, please see here. For more information on the NCUA share insurance fund, please see here. You are solely responsible for monitoring the amount of funds you have on deposit at each a Product Bank, whether through the Raisin platform or outside the Raisin platform, to confirm that the deposits you hold in the same capacity at each Product Bank do not exceed the maximum deposit insurance coverage provided by the applicable Deposit Insurer.