SMART financial goals: Things to consider

What you need to know about tracking and setting SMART financial goals.

Key takeaways

: Using the SMART money goals framework can help you set .

: Break larger SMART financial goals into , and adjust as needed.

: When setting SMART financial goals, avoiding common mistakes such as unrealistic expectations, lack of planning, and failure to align goals with your budget can help you better reach your goals.

What are SMART financial goals?

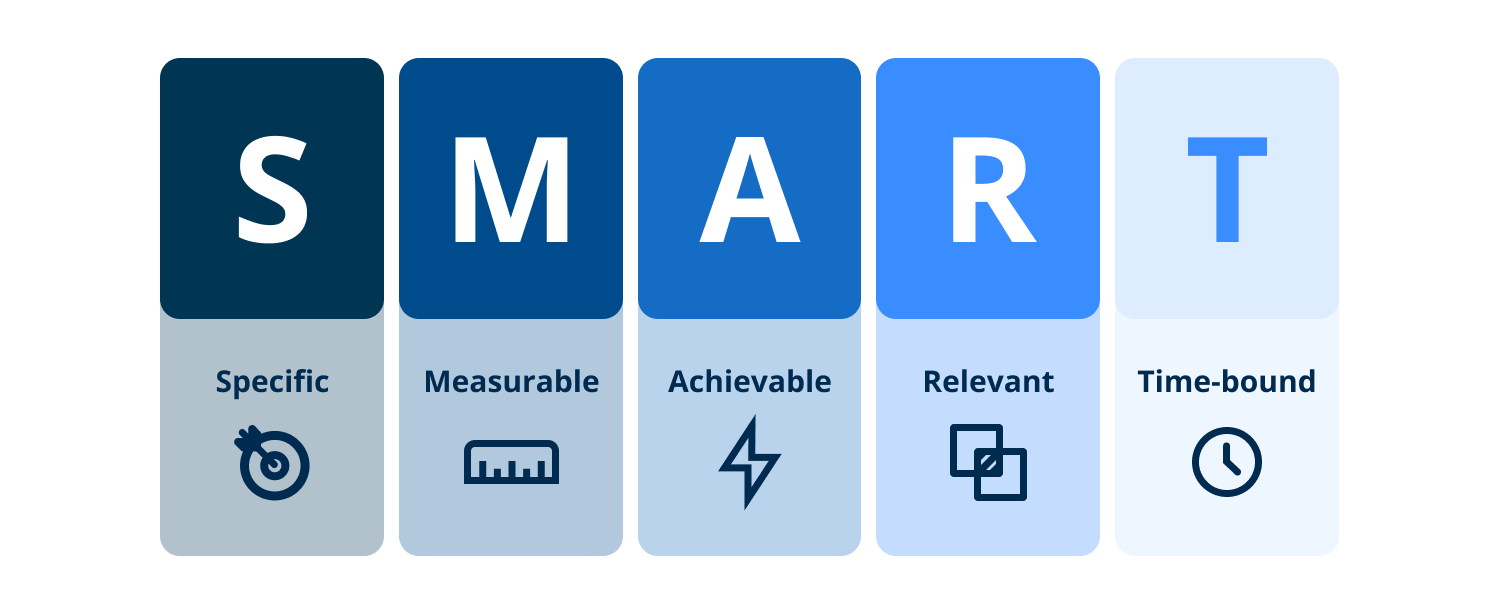

SMART financial goals are a tested method for setting clear, attainable objectives that help you stay focused and organized when managing your finances. The SMART acronym stands for Specific, Measurable, Achievable, Relevant, and Time-bound. Using this framework of setting SMART financial goals can guide your decision-making process, provide structure, and increase your chances of success.

Each element of the SMART money goals helps you learn more about managing your savings efficiently. This is how they might apply to your personal financial progress:

S – Specific: The goal should be well-defined and clear. A vague goal like “I want to save money” is less effective than “I want to save $6,000 for a down payment for a car.” Being specific helps you visualize the goal and outline the steps to reach it.

M – Measurable: You need a way to quantify and measure your goal. Tracking your savings or debt payments can help you measure progress. For example, “Save $200 per month” or “Pay off $1,000 in credit card debt by making $100 payments each month.”

A – Achievable: Consider whether your SMART financial goal is realistic based on your income, expenses, and financial situation. Overly ambitious goals can lead to frustration, so you might want to start with small, achievable wins and build momentum.

R – Relevant: Your financial goal should align with your current life stage, values, and broader objectives. Whether it is saving for retirement, creating an emergency fund, or reducing (credit card) debt, the goal should support your long-term financial wellbeing.

- T – Time-bound: Set a clear deadline to complete the goal. A time frame creates urgency and accountability. For instance, “Save $3,000 for a vacation in nine months” provides a specific target date to work toward.

How to set SMART financial goals

By setting SMART financial goals, you are actively designing a roadmap helping you reach your goals, because you are learning how to achieve the progress you desire. SMART financial goals start with understanding where you are now, learning where you want to go, and creating a clear, realistic plan to get there.

Before you can set effective SMART money goals, take time to review your current financial situation. This means looking at your income, expenses, outstanding debts, and savings. Knowing your numbers — how much you earn, spend, and owe — can provide a good starting point for responsible goal-setting.

Once you understand your financial baseline, you may want to shift your focus to learning more about your priorities and useful strategies for achieving them. Examples of SMART financial goals vary widely depending on your life stage, family structure, values, and personal desires. It is often helpful to break SMART financial goals down into three categories: short-term, mid-term, and long-term goals.

Once your goals are broadly outlined, you can go through each one and ask yourself:

Is it specific enough to take daily, weekly, or monthly action toward?

Can I measure my progress over time?

Is it realistic based on my current income, expenses, savings, and obligations?

Does it reflect something that matters to me personally or professionally?

Have I set a deadline or timeframe to complete it?

SMART financial goals: Examples

Listing your SMART money goals allows you to visualize your financial priorities and clarify what progress looks like. However, simply naming your goals is not enough. The real power comes from turning these intentions into SMART financial goals.

Examples of SMART financial goals have to be specific and actionable. Goals like “save more money” or “get out of credit card debt” are too vague to guide your daily actions. On the other hand, saying “Save $5,000 for a vacation over 10 months by setting aside $500 each month” gives you a clear target, timeline, and plan for action.

SMART financial objectives: Examples

Timeframe: | Duration: | Examples: |

Short-term | 0–1 year | Paying off high-interest credit card debt to reduce stress and increase cash flow, saving for a wedding, vacation, or emergency fund |

Mid-term | 1–5 years | Building a down payment for a home, purchasing a new car, starting a business or preparing for a major life change (e.g., relocation) |

Long-term | 5+ years | Contributing regularly to a retirement fund (e.g., 401(k), IRA), creating a college fund for your child, becoming financially independent or paying off a mortgage early |

Here is another great example of a SMART financial goal that meets all five criteria: "Save $1,200 for a new laptop in six months by setting aside $200 per month from my paycheck."

Specific: The goal is clear — save for a new laptop.

Measurable: The total amount and monthly contributions are defined.

Achievable: Based on the person’s income, saving $200 per month is realistic.

Relevant: The goal aligns with a current need or desire.

Time-bound: There is a six-month deadline, creating a sense of urgency.

This is a classic textbook example of how to turn a vague intention into a well-structured, SMART financial goal. By applying the same approach to your own priorities — whether it is savings, budgeting, or debt reduction — you will probably see progress in a short amount of time.

Tips to achieve your SMART money goals

Once your SMART financial goals are set, the next step is making steady progress. Here are some strategies to help make it easier to stay on track:

Start a savings account

Savings accounts are a great way to help keep you accountable when it comes to reaching your SMART goals. Savings accounts can also help diversify your savings, and options like high-yield savings accounts can help you reach your financial goals even faster.

The Raisin marketplace gives you access to high-yield savings options with competitive interest rates, to help you smash your savings goals. Explore different savings options and start reaching your goals today!

Financial goal chart

Visualizing your progress with a financial goal chart can be incredibly motivating and rewarding. These charts allow you to see where you started, how far you have come, and how much further you need to go to reach your goal. Whether you use a digital app, a spreadsheet, or a printed goal tracker, the visual representation can help make your efforts feel more tangible.

Break goals into smaller pieces

Large SMART money goals can feel overwhelming, which can make it harder to take the first step. Breaking them into smaller, manageable pieces makes them more achievable and less stressful. This approach helps make progress feel more attainable and encourages you to stay consistent with your efforts.

Stay accountable

Accountability is a powerful motivator when it comes to reaching your SMART financial goals. Sharing your goals with a trusted friend, family member, or financial advisor can increase your commitment and follow-through. You can also set personal reminders or use budgeting apps that send notifications and track your actions.

Celebrate your success

Celebrating milestones along the way helps maintain motivation and reinforces positive habits. Whether you have reached a small benchmark or reached your SMART money goal, recognition matters. Choose rewards that are meaningful but budget-friendly, like a special meal or a fun outing.

Common mistakes to avoid

Even after setting SMART financial goals, it can be easy to go off course. Life can be unpredictable, and without a thoughtful approach, financial goals can become forgotten or feel unachievable.

Setting unrealistic goals

Ambition is great, but setting SMART financial goals that far exceed your financial capacity can lead to burnout and discouragement. While your SMART money goals should challenge you, they must also be realistic based on your actual financial situation. Focus on attainable milestones that can help you stick to your savings resolutions.

Not having a plan

Identifying a SMART financial goal is an important start, but it is only part of the equation. Without a clear, structured plan of action, even the most well-defined goals can stagnate. It can help to break down each goal into small, achievable steps and setting deadlines. Being time-bound allows you to remain focused and to measure consistent progress.

Disregarding your budget

You might be excited to fund a vacation or build a home down payment, but if your current budget does not support regular contributions, the SMART money goal may quickly fall apart. Are you wondering how to budget money efficiently? Make sure you account for all fixed and variable expenses when calculating how much you can realistically allocate each month.

Not tracking your progress

If you do not track your progress, it is easy to lose momentum or forget your original target altogether. Regular check-ins help ensure you are still on track to reach your financial goals. Tracking your progress also helps you spot patterns, like overspending or inconsistent saving habits, that might be interfering with your progress. Features like spreadsheets, budgeting apps, or visual charts can help you stay engaged.

Bottom line

If you are ready to take control of your financial future, setting SMART financial goals is a powerful first step. This framework helps you create clear, achievable objectives that fit your budget and priorities. Whether saving for a down payment, paying off debt, or funding retirement, SMART financial goals can help you stay motivated and on track.

To support your SMART money goals, the Raisin marketplace is here to help. Raisin gives you access to various high-yield savings products, to help make the most of your savings. Sign up today and start watching your savings grow.

The above article is intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law, or any other business and professional matters that affect you and/or your business.

Related Content

© 2026 Raisin SE. All rights reserved.

The Raisin name and logo are trademarks of Raisin SE. All other trademarks, logos, marks, and brand names are the property of their respective owners.

*APY means Annual Percentage Yield. APY is accurate as of July 24, 2026. Interest rate and APY may change after initial deposit depending on the terms of the specific product selected. Minimum opening deposit is $1.00.

Raisin is not an FDIC-insured bank, and FDIC deposit insurance only covers the failure of an insured bank.

Raisin is not an NCUA-insured credit union. NCUA deposit insurance only covers the failure of an insured credit union.

Raisin does not hold any customer funds. Customer funds are held in various custodial deposit accounts. Each customer authorizes the Custodial Bank to hold the customer’s funds in such accounts, in a custodial capacity, in order to effectuate the customer’s deposits to and withdrawals from the various bank and credit union products that the customer requests through Raisin.com. The Custodial Bank does not establish the terms of the bank or credit union products and provides no advice to customers about bank or credit union products offered by the applicable bank or credit union through Raisin.com. Each customer also authorizes the Service Bank to move funds among the various banks and credit unions at the customer’s request. First International Bank & Trust (FIBT), Member FDIC, is the Service Bank. Bell Bank and Starion Bank, each Member FDIC, are the Custodial Banks.

†Based on $250,000 in FDIC or NCUA insurance coverage per insurable category of ownership at each partner bank or credit union on the Raisin platform (each a "Product Bank"), when aggregated with all other deposits held by you at such Product Bank and in the same insurable category. Deposits made through Raisin will be eligible to receive deposit insurance from the FDIC or the NCUA (each a "Deposit Insurer") in accordance with and up to the maximum amount permitted by law at each Product Bank. Raisin is not a bank or credit union and does not hold any customer funds. Funds are held at FDIC-insured banks and NCUA-insured credit unions. Deposit insurance covers the failure of an insured bank or credit union. Certain conditions must be satisfied for pass through deposit insurance coverage to apply. Customers may choose to deposit funds with identically registered accounts at different Product Banks on the Raisin platform to be eligible for Deposit Insurer coverage up to $10 million for individual accounts and $20 million for joint accounts when at least 40 Product Banks are utilized. Please be aware, however, that any deposits you have at a Product Bank, whether through the Raisin platform or outside the Raisin platform, that you may hold in the same capacity (such as in an individual capacity or joint capacity) count toward the applicable Deposit Insurer's deposit insurance maximum amount, and any such amounts that you hold in the same capacity at a Product Bank that exceed the maximum insurance coverage by the applicable Deposit Insurer will not be insured. For more information on FDIC deposit insurance, please see here. For more information on the NCUA share insurance fund, please see here. You are solely responsible for monitoring the amount of funds you have on deposit at each a Product Bank, whether through the Raisin platform or outside the Raisin platform, to confirm that the deposits you hold in the same capacity at each Product Bank do not exceed the maximum deposit insurance coverage provided by the applicable Deposit Insurer.