What is a stock market correction?

Understanding market corrections and their impact

Key takeaways

A 10-20% decline in the market from a recent peak, often due to shifts in the economy, Federal Reserve rates, geopolitical tensions, or overvalued stocks.

They usually recover within a few months. Prolonged declines could signal a bear market or recession.

Investors might look to build diversified portfolios, including options like ETFs or equal-weighted indices, or even locking in high interest rates with CDs.

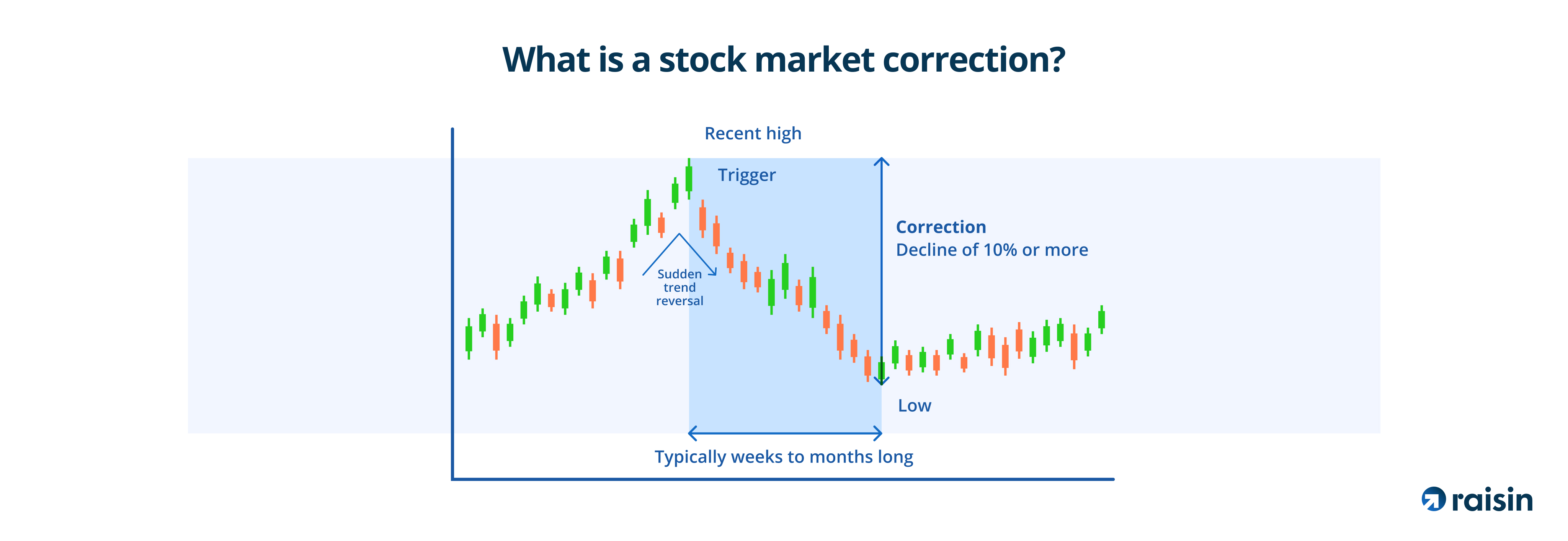

What is a correction in the stock market?

A stock market correction happens when the price of a stock, asset, or even an entire financial market drops 10% or more (but no more than 20%) from a recent peak. This often happens across major sectors and indexes like the Dow Jones or the S&P 500, but the key feature is how big the decline is — this is what defines a market correction.

To put it in context, there are different levels of market declines. A smaller drop of less than 10% is called a “dip” and is a fairly normal part of the market’s daily fluctuations. If the decline continues past 20%, it’s known in investment speak as a “bear market” or a “crash.” Media headlines sometimes play up stock market corrections as “crashes” to grab the attention of readers.

What causes a stock market correction?

Market corrections don’t come out of nowhere; they’re often sparked by political uncertainty, economic shifts, or global crises, such as war. When investors are spooked by reports of a slowing economy or other news relevant to their investments, they’re more likely to sell their stocks than buy new ones, which drives down the market.

Federal Reserveinterest rate changes can also contribute to a market falling into correction territory. When rates go up to combat inflation, borrowing becomes more expensive. As a result, the economy cools, which triggers sell-offs.

While stock market corrections can make investors uneasy, they’re technically a normal and healthy part of the market’s cycle. After all, what goes up must come down. Sometimes, stock prices get too high, too quickly, and a correction is just the market’s way of leveling things out. It helps restore balance in the markets and bring prices back to their typical levels.

How long does it take to recover from a stock market correction?

A stock market is considered to have left correction territory once the financial market starts hitting new highs after its period of decline. Market corrections are usually short-lived, lasting anywhere from a few weeks to a few months, and are often followed by strong rebounds. Of course, it’s also possible they end up continuing their downward trend and develop into a bear market, which takes longer to recover from.

Looking at data from the S&P 500, the market tends to bounce back relatively quickly after a decline. On average, it takes about three months to recover from a smaller dip of 5% to 10%, and around eight months¹ for a more significant stock market correction. But if a recession occurs, the market can decline further and may take years to fully recover.

When was the last stock market correction?

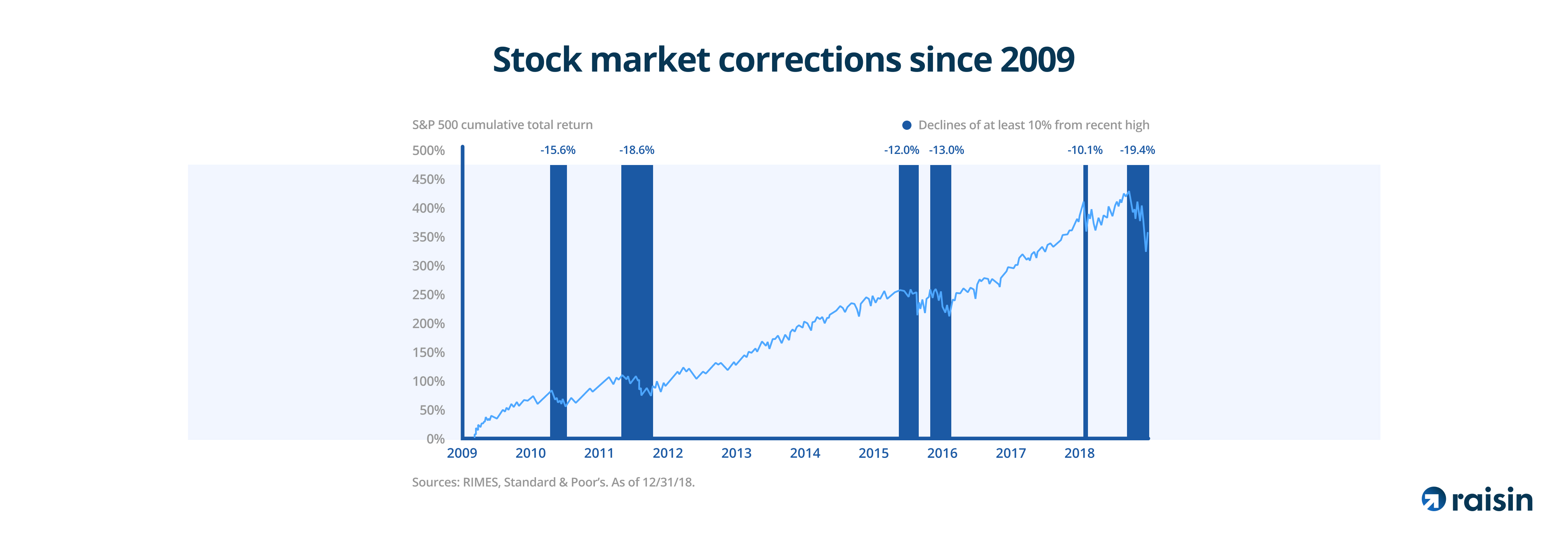

When you think of stock market downturns, recent major upheavals like the Covid-19 pandemic in 2020 or the 2008 financial crisis might come to mind. These were instances of bear markets tied to recessions of varying intensities, and they’re relatively rare.

Stock market corrections, on the other hand, happen more often than you might expect. In fact, there have been corrections in several of the past 20 years alone.

Corrections have also been seen more recently in 2024. The NASDAQ Composite — an index that tracks tech companies — officially entered correction territory in August, dropping 13% from its peak in early July. The S&P 500 came close too, falling 8.5% from its mid-July high.

Because the markets are resilient and tend to rally after a few months, stock market corrections don’t always make the headlines, but they aren’t uncommon.

Is a stock market correction coming?

Predicting whether a stock market correction might be on the horizon is challenging, even for the most seasoned investors and economists. Various factors can trigger dips, and it’s hard for anyone to anticipate what might happen in the future.

Financial experts have nevertheless identified signs that could indicate potential market volatility. They point to data showing higher than expected unemployment rates and ongoing geopolitical tensions.

In general, investors have their eyes on trends in the labor market and possible changes to interest rates. If unemployment increases, the Fed could respond by lowering interest rates to boost the economy. This, in turn, could result in greater market volatility.

Should you buy stocks during a market correction?

When the market falls during a stock market correction, investors might be tempted to scoop up some shares at lower prices. But landing a bargain investment deal won’t necessarily pay off in the long run. Investors might instead seek out companies that are recording consistent growth in their annual profits. Generally, if a company is thriving, there’s a good chance its stock price will follow suit over time.

So while a market correction can offer investment opportunities, it can also be worth looking at the company’s overall financial health and long-term growth potential, rather than just chasing cheaper stocks.

What should investors do during a stock market correction?

Investments are intended as a long-term venture. Panicking and selling stocks at the first sign of volatility in the markets can prevent investors from riding out any turbulence and seeing potential growth in their funds later down the line.

Of course, your particular course of action will depend on where you are in your investment journey. New investors may have time on their side to ride out any peaks and troughs. Those approaching retirement or coming closer to needing the funds for a savings goal may take a more cautious approach, as there’s less time to weather future market dips.

Managing risk during a stock market correction

As we’ve seen, stock market corrections are fairly common and usually temporary, but that doesn’t make them any less nerve-wracking for investors.

Here are a few other ways that could help manage risk during market downturns:

- Diversification: Building a diversified portfolio is one of the most common strategies for managing risk. By spreading investments across different assets, the overall risk of loss is reduced. This means not putting all investments in a single asset class, industry, or company. Even cash can play a role in diversification.

- Exchange-Traded Funds (ETFs): ETFs can help spread risk by giving investors exposure to a variety of assets, rather than just one or two companies. This diversification can prevent investors from having to rely on the performance of individual stocks.

- Equal-weighted index: This is a specific type of ETF, such as the S&P 500 Equal Weight Index. This index treats all 500 companies equally, giving smaller companies the same weight as the larger ones. Unlike the S&P 500, where larger companies dominate the index, this approach can potentially reduce the impact of larger companies struggling in the short term.

- Lock in high interest rates with certificates of deposit (CDs): With potentially more interest rate cuts in the pipeline, opening a CD now could be an effective way to lock in higher interest at current rates. That way, you have guaranteed returns for a set period, even if rates fall in the future.

When managing investments during a market correction, it is often recommended to be mindful of your financial goals, and remember why you chose this route in the first place. Experts often advise against letting any emotional reactions drive decisions, and instead stress the importance of focusing on the bigger picture. Investing always carries risk, however, and there’s no guarantee you’ll get back your original investment.

Putting your money to work risk-free with Raisin

If you’d rather avoid the inherent risk and volatility that comes with investing in the stock markets, savings accounts such as high-interest CDs can offer a potentially safer alternative.

As a one-stop savings platform, Raisin makes it easy for savers to explore a range of options, all in one free login. With access to high-yield CDs, no-penalty CDs, and more from over 70 federally regulated banks and credit unions, it’s a simple way to get more from your savings.

The above article is intended to provide generalized financial information designed to educate a broad segment of the public; it does not give personalized tax, investment, legal, or other business and professional advice. Before taking any action, you should always seek the assistance of a professional who knows your particular situation for advice on taxes, your investments, the law, or any other business and professional matters that affect you and/or your business.

Related Content

© 2026 Raisin SE. All rights reserved.

The Raisin name and logo are trademarks of Raisin SE. All other trademarks, logos, marks, and brand names are the property of their respective owners.

*APY means Annual Percentage Yield. APY is accurate as of April 8, 2026. Interest rate and APY may change after initial deposit depending on the terms of the specific product selected. Minimum opening deposit is $1.00.

Raisin is not an FDIC-insured bank, and FDIC deposit insurance only covers the failure of an insured bank.

Raisin is not an NCUA-insured credit union. NCUA deposit insurance only covers the failure of an insured credit union.

Raisin does not hold any customer funds. Customer funds are held in various custodial deposit accounts. Each customer authorizes the Custodial Bank to hold the customer’s funds in such accounts, in a custodial capacity, in order to effectuate the customer’s deposits to and withdrawals from the various bank and credit union products that the customer requests through Raisin.com. The Custodial Bank does not establish the terms of the bank or credit union products and provides no advice to customers about bank or credit union products offered by the applicable bank or credit union through Raisin.com. Each customer also authorizes the Service Bank to move funds among the various banks and credit unions at the customer’s request. First International Bank & Trust (FIBT), Member FDIC, is the Service Bank. Bell Bank and Starion Bank, each Member FDIC, are the Custodial Banks.

†Based on $250,000 in FDIC or NCUA insurance coverage per insurable category of ownership at each partner bank or credit union on the Raisin platform (each a "Product Bank"), when aggregated with all other deposits held by you at such Product Bank and in the same insurable category. Deposits made through Raisin will be eligible to receive deposit insurance from the FDIC or the NCUA (each a "Deposit Insurer") in accordance with and up to the maximum amount permitted by law at each Product Bank. Raisin is not a bank or credit union and does not hold any customer funds. Funds are held at FDIC-insured banks and NCUA-insured credit unions. Deposit insurance covers the failure of an insured bank or credit union. Certain conditions must be satisfied for pass through deposit insurance coverage to apply. Customers may choose to deposit funds with identically registered accounts at different Product Banks on the Raisin platform to be eligible for Deposit Insurer coverage up to $10 million for individual accounts and $20 million for joint accounts when at least 40 Product Banks are utilized. Please be aware, however, that any deposits you have at a Product Bank, whether through the Raisin platform or outside the Raisin platform, that you may hold in the same capacity (such as in an individual capacity or joint capacity) count toward the applicable Deposit Insurer's deposit insurance maximum amount, and any such amounts that you hold in the same capacity at a Product Bank that exceed the maximum insurance coverage by the applicable Deposit Insurer will not be insured. For more information on FDIC deposit insurance, please see here. For more information on the NCUA share insurance fund, please see here. You are solely responsible for monitoring the amount of funds you have on deposit at each a Product Bank, whether through the Raisin platform or outside the Raisin platform, to confirm that the deposits you hold in the same capacity at each Product Bank do not exceed the maximum deposit insurance coverage provided by the applicable Deposit Insurer.