Klarna Bank

2.72 %AER

If you’re hoping to retire early, you’re not alone. Almost three-quarters of Ireland’s working population aspire to retire at or before age 60.

On this page, you’ll discover what early retirement in Ireland could look like, including implications for your pension, pros and cons, and how much money you might need. We’ll also explore practical steps you can take to help you work towards the goal of retiring early, like setting up a high-interest savings account.

You can usually draw occupational pensions from age 50 after leaving the employment tied to the scheme (subject to trustee consent). Personal pensions and PRSAs generally unlock at age 60, though early access to a PRSA is possible from age 50 if you are retiring from PAYE employment.

After taking early retirement in Ireland, you can often access up to 25% of your pension fund as a tax-free lump sum.

You can take steps to prepare for early retirement by creating a budget, maximising pension contributions, and reviewing savings strategies.

The information provided here is for informational and educational purposes only and does not constitute financial advice. Please consult with a licensed financial adviser or professional before making any financial decisions. Your financial situation is unique, and the information provided may not be suitable for your specific circumstances. We are not liable for any financial decisions or actions you take based on this information.

Early retirement means stepping away from work before you reach the standard State Pension age. In Ireland, the minimum age to claim the State Pension is currently 66, though you now have the flexible option to defer claiming it up to age 70 in exchange for higher payments.

You might decide to retire early, or it could happen unexpectedly if you are made redundant or face health issues. The typical early retirement age in Ireland ranges from 50 to 65. Your exact options will depend on your employment contract and the rules of your specific pension scheme.

Leaving the workforce ahead of schedule means you will have an income gap before your state benefits begin. You will need to rely on your personal savings and private pensions to fund your lifestyle during these years. This requires careful preparation to ensure your money lasts for a longer period of time.

The exact age you can retire depends on the type of pension plan you hold, and any additional funds you have to support your retirement.

Most occupational pension schemes allow you to take early retirement from age 50, provided you have left that specific employment. You will generally need the consent of the pension trustees, and sometimes your employer, to do this.

If you hold a Personal Retirement Savings Account or a personal pension, the standard statutory access age is 60. However, an exception exists allowing you to access your PRSA from age 50 if you are retiring from PAYE employment.

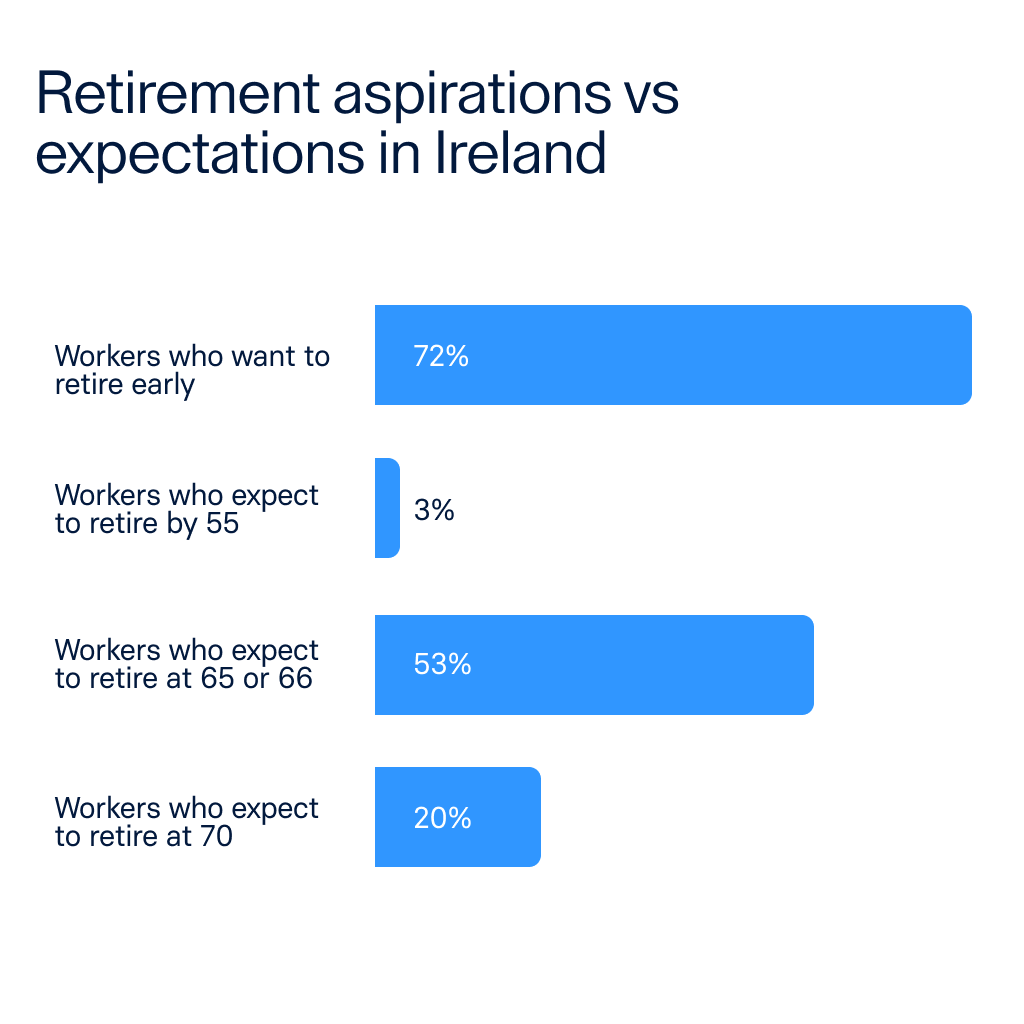

Early retirement is a popular goal, with 72% of Ireland’s working population aspiring to it. Four in 10 workers say they’d retire by the age of 50 or even sooner if they could, and a third state 60 as their ideal retirement age*. However, over half of Irish workers expect the State Pension to be their main source of income**, which would leave a gap between early retirement age and the age at which they could claim their pension at 66. When asked about the realities of retirement, just 3% of people expected to be able to retire by 55. 53% expected to leave the workforce when they reached State Pension age, or just before. 20% said they would not be able to retire until the age of 70***.

*https://www.royallondon.ie/press-releases/2025-press-releases/March/ideal-retirement-age-March-2025/

**https://www.cso.ie/en/releasesandpublications/ep/p-pens/pensioncoverage2024/keyfindings/

***https://www.royallondon.ie/press-releases/2025-press-releases/april-2025/predicted-retirement-age-April-2025/

Early retirement depends on solid financial planning to create income options that can bridge the gap between retirement and State Pension age, and help create the lifestyle you want in retirement. A growing number of people are followers of the Financial Independence Retire Early (FIRE) movement, which suggests that by aggressively saving and investing, you could retire as early as your 40s.

From a practical perspective, many employment contracts in Ireland set a retirement age, typically around 65. However, depending on your employer and scheme rules, you may have the option to take early retirement and access your occupational pension from age 50, provided you leave the company. Early retirement in the public sector has different rules to the private sector. So if you’re wondering how early you can retire, a first step might be to check your employment terms to see what’s possible for you.

As an example, if you wanted to retire at 60, you would need to calculate the income gap between age 60 and the State Pension age at 66. This means you need six years of fully self-funded living expenses.

Calculation Example: If you determine you need €30,000 per year to live comfortably, you would multiply this by the six years until your State Pension begins.

€30,000 x 6 years = €180,000.

With this example, you’d need at least €180,000 in accessible savings or private pension income to bridge the gap until you reach age 66. You may also want additional income once you begin receiving your State Pension, as inflation can reduce the purchasing power of your money over time.

Sometimes, early retirement isn’t a choice you make, but a necessary decision if you become ill while still employed. If you’re under 66 and have to permanently stop working due to ill health, you may be eligible to apply for the Invalidity Pension. This is a long-term payment based on your PRSI contributions, which automatically transfers to the State Pension when you reach 66. For shorter-term illnesses, the Illness Benefit may apply, though this is typically capped at one or two years.

If you take early retirement due to ill health,you may be eligible to receive your pension immediately, and in some cases, you may receive notional added years. These are additional years credited to your pension record, even though you didn’t actually work them.

Terms and conditions of early retirement due to ill health vary by pension scheme. In a defined benefit scheme, you may receive full benefits at normal retirement age, providing immediate financial support. However, in a defined contribution scheme or personal pension plan, retiring early could reduce your annual income.

Cost-Neutral Early Retirement (CNER) is a way for public servants to retire early in Ireland and get their pension before their preserved (standard) pension age, which is typically 60 or 65. Under this arrangement, eligible employees can retire between the ages of 50 and 60, depending on when they started working. The pension amount will then be reduced to account for the early payment and longer payment duration.

To be eligible for CNER, you have to meet certain requirements. Firstly, you should be working for a public service organisation and be a member of their pension scheme. CNER is an option open to most standard public servants, including teachers, nurses, and clerical officers. Secondly, you must have the right to receive your pension at either age 60 or 65, depending on your scheme. Finally, you should apply for CNER and complete the HSE early retirement form before you retire.

If you’re considering early retirement in Ireland, you may be wondering whether you can cash in a pension early. The main requirement is that you must have left the job where you built up your pension, and you must have been employed in the private sector.

The rules for early access to pensions vary depending on the type of pension scheme you have:

With most schemes, you can access up to 25% (up to a maximum of €200,000) of your pension fund as a tax-free lump sum, but income tax applies to the rest. Occupational pension schemes let you take a lump sum based on your salary and years of service.

After taking a lump sum from your pension upon retirement, you have options such as paying for an annuity or transferring the rest of your pension into an Approved Retirement Fund (ARF). An annuity offers payments over a specific period of time, providing a guaranteed income stream. On the other hand, an ARF can provide more flexibility in managing retirement funds.

You might find it helpful to get advice from a financial adviser to understand the specific rules around early pension withdrawal in Ireland and what it would mean for you.

Deciding to retire early is a major financial step. It can help to weigh the lifestyle benefits against the financial realities.

You might start by thinking about how you plan to live your life as you age, and whether your savings will be enough to sustain that lifestyle. Looking ahead, you might also factor in unexpected expenses, healthcare costs, and inflation over a potentially longer retirement period.

Here are some of the pros and cons of early retirement:

Pros of early retirement | Cons of early retirement |

More time to travel and pursue hobbies | A smaller overall pension pot |

More time to focus on your health | Higher risk of outliving your savings |

Opportunity to start a new career or business | A smaller tax-free lump sum |

More time to spend with family and friends | Inflation could reduce your purchasing power over a longer period |

If you’re considering early retirement, you might want to consult your pension provider for precise details on exactly how your pension fund would be affected. Taking early retirement in Ireland without continued employment may create PRSI contribution gaps, impacting your entitlement to the State Pension. However, you might be able to bridge this gap by obtaining credits or making voluntary contributions, so you would still qualify for the State Pension.

There are some useful tools like pension calculators to help you assess if you’re on track to meet your target pension payment based on your current contributions and the age you aim to retire.

If you choose to leave the workforce early in Ireland, you might still qualify for Jobseeker’s Benefit or Jobseeker’s Allowance. However, because early retirement is considered voluntarily leaving your job, you will typically face a 9-week disqualification period before payments begin. Crucially, unless you are claiming the specific 'Benefit Payment for 65 Year Olds', you must still be capable of, available for, and genuinely seeking full-time work to legally claim standard Jobseeker's payments.

Here are some ways you might begin your journey towards early retirement:

With over 30 European partner banks offering competitive rates on savings accounts, including fixed term deposit accounts and demand deposit accounts, Raisin offers plenty of choice if you’re considering early retirement in Ireland and looking for ways to grow your savings.

Once you’re registered, simply log in to apply for free in just a few clicks.

© 2026 Raisin Bank AG, Frankfurt a.M.

All interest rates displayed are Annual Equivalent Rates (AER), unless otherwise explicitly indicated. The AER illustrates what the interest rate would be if interest was paid and compounded once a year. This allows individuals to compare more easily what return they can expect from their savings over time. Raisin Bank, trading as Raisin, is authorised/licensed or registered by BaFin (Bundesanstalt für Finanzdienstleistungsaufsicht) in Germany and is regulated by the Central Bank of Ireland for conduct of business rules.